Many business owners believe that improving working capital efficiency requires cutting costs or borrowing more. But what if we told you there’s a smarter way to optimize your cash flow without adding debt or slashing your budget? There is. It’s invoice factoring. Below, we’ll walk you through how to leverage factoring for working capital efficiency and build a stronger, more sustainable business.

The Basics of Working Capital Efficiency

Working capital efficiency relates to how effectively your business manages its day-to-day financial resources. In short, it’s the cash you have on hand to cover short-term obligations, like paying employees, suppliers, and overhead expenses. Implementing invoice factoring for cash efficiency is essential for maintaining a healthy financial balance.

Why Working Capital Efficiency is Important

Working capital efficiency impacts your business’s ability to operate smoothly. If you’re managing working capital efficiently, you’ll have enough liquidity to handle unexpected expenses, take advantage of growth opportunities, or invest in inventory when demand spikes. On the other hand, poor working capital management can lead to cash shortages, missed growth opportunities, or even the inability to meet critical financial obligations.

For example, the average small business only has enough cash to cover 27 days of expenses, according to JP Morgan surveys. Industries like wholesale and construction come in even lower, at 23 days and 20 days, respectively. These slim margins show just how crucial efficient working capital management is—without it, you might be forced into expensive borrowing or delay crucial investments, which can stunt growth.

The Basics of Invoice Factoring

Invoice factoring is a financial tool that helps businesses unlock the cash tied up in their unpaid invoices. Instead of waiting 30, 60, or even 90 days for customers to pay, you can sell those invoices to a factoring company for immediate cash. This is particularly useful if you’re running a business that offers payment terms to clients but still needs consistent cash flow to cover everyday expenses. Invoice factoring for cash efficiency offers a flexible way to access funds without incurring debt.

The Process of Invoice Factoring Explained

Now, let’s walk through the step-by-step process of invoice factoring.

Step 1: Submit Your Unpaid Invoice

First, once you’ve completed your work or delivered a product, you issue an invoice to your customer as usual. Rather than waiting for them to pay, you submit that unpaid invoice to a factoring company.

Step 2: Factoring Company Assesses the Invoice

The factoring company reviews the invoice and checks the creditworthiness of your customer. They aren’t as concerned about your credit, but they’ll want to ensure that your customer is likely to pay the invoice on time. This helps ensure capital efficiency by reducing the risk of non-payment.

Step 3: Receive a Cash Advance

Once approved, the factoring company advances you a portion of the invoice’s value—typically around 60 to 95 percent. You get that cash quickly, often within 24-48 hours, though some factoring companies offer same-day payments.

Step 4: Customer Pays the Factoring Company

Your customer then pays the full amount of the invoice directly to the factoring company according to the original payment terms.

Step 5: Final Payment Minus Fees

Once the customer pays, the factoring company releases the remaining balance of the invoice to you, minus their fees. Fees generally range from one to five percent of the invoice value, depending on factors like the customer’s creditworthiness and the length of the payment terms. Short-term financing through factoring like this helps businesses maintain a consistent flow of capital.

Benefits of Invoice Factoring

The main benefit of invoice factoring is that it bridges the cash flow gap created by delayed payments. If you’ve ever had to chase down late payments or struggled with a tight budget because your customers haven’t paid on time, you know how stressful it can be. Factoring as a financial solution addresses this by giving you access to funds within a matter of days, not weeks or months. Optimizing liquidity with invoice factoring can be especially critical during periods of growth or financial stress.

For instance, a manufacturing company that’s waiting for large corporate customers to pay might struggle to purchase materials or pay employees in the meantime. With factoring, they can sell those invoices and receive immediate cash to keep production going without interruption.

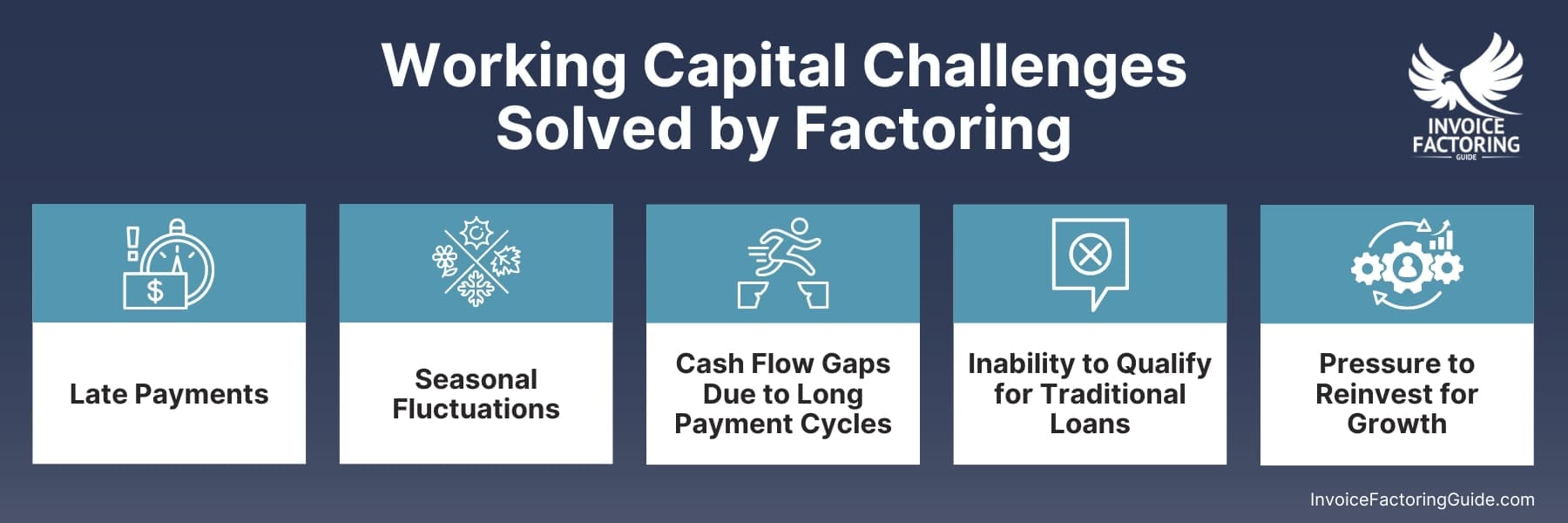

Working Capital Challenges Solved by Factoring

Due to the unique way factoring works, it addresses many different types of working capital challenges.

Late Payments

One of the most frustrating issues for any business is dealing with late payments from customers. Even if you have reliable clients, payment terms like net 30 or net 60 mean you’re waiting a month or two for cash. If customers delay beyond those terms, it puts even more strain on your cash flow.

Factoring allows you to turn those unpaid invoices into immediate cash. Rather than waiting for customers to pay, you get access to most of the invoice amount within days of issuing it. This frees up funds to cover operating expenses, payroll, and growth initiatives without having to borrow or dip into savings. It also improves accounts receivable and capital efficiency by converting pending payments into working capital, helping businesses maintain smooth operations. Factoring services for working capital ensure that your business can operate without the stress of waiting on payments.

Your factoring company will also run credit checks on your customers and provide insights about how much trade credit can be extended. This helps ensure clients who receive trade credit are likely to pay in full and on time.

Seasonal Fluctuations

Many businesses experience peaks and valleys in revenue due to seasonality. For example, retail, agriculture, and manufacturing sectors often have busy seasons followed by slow periods. Managing working capital during off-seasons can be a struggle, especially when cash is tied up in unpaid invoices.

Factoring provides a steady stream of cash, even when business is slow, increasing operational cash with factoring and ensuring your business can cover expenses and seize new opportunities. By factoring invoices during peak seasons, you can build up a cushion to carry you through slower months. Plus, you can quickly ramp up cash flow if unexpected opportunities arise, such as purchasing inventory for a last-minute rush or covering payroll during the off-season. Overcoming cash flow challenges with factoring gives businesses the flexibility they need to navigate seasonal cycles.

Cash Flow Gaps Due to Long Payment Cycles

Businesses that serve large corporations or government entities often have to deal with long payment cycles. While waiting for payments, you still need to pay your own vendors, employees, and overhead costs. This creates a significant cash flow gap, especially for small businesses.

Factoring eliminates that cash flow gap by providing fast access to cash tied up in those long-term invoices. This enables businesses to keep operations running smoothly, even when waiting for large clients to pay.

Inability to Qualify for Traditional Loans

Many small businesses, especially startups or companies with limited credit histories, find it difficult to qualify for traditional loans or lines of credit. Even if they are approved, the process can take weeks, and they may not receive the full amount they need.

Factoring is based on the creditworthiness of your customers, not your business’s credit score. This makes it a more accessible financing option for companies that may not qualify for bank loans. Plus, the approval process is faster, often just a couple of days, so you can get the cash when you need it most. Alternative financing options for businesses, such as factoring, offer an efficient way to meet cash flow needs without incurring debt.

Pressure to Reinvest for Growth

Growing businesses need to reinvest in inventory, marketing, technology, and talent, but cash flow constraints can make it hard to fund expansion. Waiting for customers to pay can cause delays in these critical investments, leading to missed growth opportunities.

Factoring gives you access to cash as soon as you issue invoices, enabling you to reinvest in your business immediately. This allows you to take advantage of growth opportunities, such as purchasing inventory for a big order or scaling up your workforce to meet demand. Leveraging factoring for financial flexibility allows businesses to make the most of growth opportunities as they arise.

Factoring vs. Traditional Financing Options

When exploring funding options to boost your working capital, it’s essential to understand how invoice factoring compares to traditional financing methods like loans and lines of credit. Each option comes with its own advantages and trade-offs, but factoring offers unique benefits that can provide faster, more flexible cash flow solutions for your business.

Factoring vs. Business Loans

Traditional business loans are a common way for companies to secure working capital. With a traditional business loan, you borrow a fixed amount from a bank or lender and repay it over time, typically with interest. Approval for a loan depends on your business’s credit history, financial statements, and sometimes personal guarantees from the owners. Loan terms can range from months to several years.

Key Differences with Factoring

- Credit Requirements: Unlike loans, factoring isn’t based on your business’s credit score. Instead, factoring companies look at your customers’ ability to pay. This makes factoring more accessible, especially for businesses with limited credit or those just starting out.

- Repayment Structure: With a loan, you’re responsible for making regular payments regardless of how well your business is doing. With factoring, there’s no loan to repay—you’re selling your invoices, not borrowing money.

- Approval Time: Business loans can take weeks or even months to approve, depending on the lender and the amount requested. Factoring approvals, on the other hand, are often completed within a few days, giving you quicker access to cash.

- Flexibility: Loans provide a lump sum, which may not match your ongoing cash flow needs. Factoring provides cash as you generate invoices, meaning you get a steady stream of working capital without taking on debt. Quick access to working capital through factoring can help businesses decide which financing option best meets their needs.

Factoring vs. Lines of Credit

A business line of credit functions like a credit card, giving you access to a set amount of funds that you can draw from as needed. You only pay interest on the amount you use, and once you pay it back, those funds become available to borrow again. Similar to loans, banks look at your creditworthiness, financial history, and collateral when approving a line of credit.

Key Differences with Factoring

- Availability of Funds: Factoring gives you access to cash based on your accounts receivable, whereas a line of credit gives you access to a pre-set borrowing limit. However, if you need more cash than what your line of credit allows, you could hit a cap. With factoring, your ability to generate cash grows as your sales increase.

- Repayment and Interest: With a line of credit, you accrue interest on what you borrow and are responsible for monthly payments. Factoring involves no such repayment—once you sell your invoice, the responsibility shifts to the factoring company to collect from your customer.

- Creditworthiness: Securing a line of credit often requires strong credit and collateral. Factoring, by contrast, relies on your customers’ credit rather than yours, making it a better option for businesses that lack substantial assets or a strong credit history.

Factoring vs. Merchant Cash Advances (MCAs)

MCAs are lump sums provided by lenders in exchange for a percentage of future sales, usually repaid through daily or weekly automatic withdrawals from your credit card or bank transactions. They are popular because they don’t require a long approval process, but MCAs tend to come with extremely high fees.

Key Differences with Factoring

- Cost: MCAs often come with much higher fees than factoring, sometimes as high as 20 percent or more. Factoring fees, by comparison, typically range from one to five percent of the invoice value.

- Repayment Terms: MCAs require daily or weekly repayments, which can put a strain on cash flow. With factoring, there are no scheduled repayments—once the invoice is factored, the factoring company waits for the customer to pay.

- Risk of Overleveraging: Because MCAs take a percentage of your future sales, they can be riskier if your sales fluctuate. Factoring is tied directly to the invoices you’ve already generated, providing a more predictable form of funding.

Factoring vs. Asset-Based Lending (ABL)

ABL involves securing a loan or line of credit using business assets like inventory, equipment, or accounts receivable as collateral. Banks or lenders typically offer ABL to businesses with substantial tangible assets, and the amount you can borrow depends on the value of those assets.

Key Differences with Factoring

- Collateral Requirements: Factoring is solely based on the value of your accounts receivable, whereas ABL requires that you pledge other business assets, such as inventory or equipment, as collateral.

- Risk to Assets: With ABL, if you default on the loan, the lender can seize your assets. Factoring carries no such risk, as there’s no loan involved.

- Ease of Access: Asset-based loans often require lengthy due diligence and asset appraisals before approval. Factoring, in contrast, can provide quick liquidity since it focuses on the strength of your invoices.

Industries That Benefit Most from Factoring

Certain industries, particularly those with long payment cycles and high operating costs, are especially well-suited to benefit from invoice factoring. By turning unpaid invoices into immediate cash, businesses in sectors like trucking, staffing, and manufacturing can maintain steady cash flow and fuel growth without waiting for customer payments.

Trucking and Transportation

The trucking industry is one of the largest users of factoring, and for good reason. Trucking companies often face long payment cycles, with brokers and shippers typically paying 30-60 days after delivery. Meanwhile, expenses like fuel, maintenance, and driver wages need to be paid immediately, creating cash flow challenges.

Factoring enables trucking companies to convert their freight bills into immediate cash, keeping trucks on the road without delay. Many factoring companies also offer additional services like fuel advances, fuel card discounts, and load management tools, making factoring an even more valuable resource.

Staffing and Recruitment Agencies

Staffing agencies face a unique cash flow challenge: they need to pay their temporary employees weekly or bi-weekly, while their clients may take 30-90 days to pay invoices. This mismatch between outgoing payroll and incoming payments can put significant strain on working capital.

Factoring bridges this gap by allowing staffing agencies to turn unpaid invoices into immediate cash. This ensures they can cover payroll on time, maintain good relationships with workers, and continue placing employees without interruptions.

Manufacturing

Manufacturers often deal with large orders from retailers or distributors, which can result in long payment terms—sometimes up to 90 days. Meanwhile, manufacturers need to purchase raw materials, pay workers, and cover production costs. This can create significant cash flow pressure, especially for smaller manufacturers or those experiencing rapid growth.

Factoring allows manufacturers to unlock the cash tied up in unpaid invoices, providing the working capital needed to keep production lines moving. With quick access to cash, manufacturers can take on larger orders, purchase materials in bulk, and invest in equipment or labor without waiting for customers to pay.

Wholesale and Distribution

Wholesalers and distributors often operate with thin margins and must maintain a steady inventory to meet customer demand. However, the long payment terms offered to customers can lead to cash shortages, especially when inventory needs to be restocked quickly.

Factoring provides wholesalers with the liquidity to purchase new inventory, fulfill large orders, and continue operating without waiting for customer payments. This is especially valuable during high-demand periods, where immediate cash flow can be the difference between meeting or missing sales opportunities.

Construction

In the construction industry, projects can span months, and contractors often have to wait for milestone payments or completion payments from clients. Meanwhile, contractors must pay for materials, labor, and subcontractors, all of which can drain cash flow during the project timeline.

Factoring gives construction companies quick access to cash for outstanding invoices, helping them stay on top of project costs and avoid delays. This is particularly useful for small contractors who may not have large cash reserves or access to traditional financing options.

Oil and Gas

Companies in the oil and gas industry often face long payment cycles, especially when dealing with large corporations. However, day-to-day operations—such as drilling, extraction, and transportation—require significant upfront capital to keep things running smoothly.

Factoring provides oil and gas companies with fast access to cash, allowing them to meet payroll, cover fuel costs, and invest in necessary equipment while waiting for customers to settle their invoices.

Professional Services

Industries like legal, consulting, and marketing firms often provide services with long payment terms, and even longer payment delays if clients struggle with their cash flow. While waiting for payments, these firms still need to cover salaries, rent, and other overhead expenses.

Factoring provides service-based businesses with consistent cash flow, allowing them to maintain smooth operations and invest in growth without relying on credit or loans. This is particularly useful when clients have lengthy approval processes or payment cycles.

Costs Associated with Factoring

When considering invoice factoring, it’s essential to understand the costs involved so you can evaluate how it impacts your bottom line. While factoring provides quick access to cash, it does come with fees that vary depending on factors like the creditworthiness of your customers, the size of your invoices, and the payment terms. Here’s a breakdown of the typical costs associated with factoring.

Factoring Fees (Discount Rate)

The most common cost is the factoring fee, also known as the discount rate. This fee is a percentage of the total invoice amount and typically ranges from one to five percent. The fee is deducted from the reserve amount (the balance held back by the factoring company until your customer pays the invoice). The exact percentage will depend on several factors:

- Invoice Size: Larger invoices often have lower fees.

- Customer Creditworthiness: Customers with stronger credit profiles may reduce the risk for the factoring company, resulting in lower fees.

- Industry: Some industries, like trucking or staffing, may have standardized rates based on industry practices.

- Length of Payment Terms: If your customers take longer to pay, the factoring fee could increase.

For example, if you factor a $10,000 invoice with a two-percent fee, the factoring company will take $200 as their fee, leaving you with $9,800 (minus any other costs).

Advance Rate

This refers to the percentage of the invoice value that the factoring company advances to you upfront. Most factoring companies offer 60 to 95 percent of the invoice’s value right away, with the remaining portion minus fees paid once your customer settles the invoice.

For instance, with a $10,000 invoice, the factoring company might advance you $8,500 immediately if the advance rate is 85 percent. The remaining $1,500 will be paid once your customer clears the invoice, minus the factoring fee.

Additional Fees

Aside from the factoring fee, there may be other charges depending on the terms of your agreement. Common additional fees include:

- Service Fees: Some factoring companies charge a flat monthly or per-invoice fee for managing accounts receivable, credit checks, and collections. This is typically a small fee, but it adds up if you’re factoring a high volume of invoices.

- Late Payment Fees: If your customer takes longer than the agreed terms to pay the invoice, the factoring company may charge a late fee or increase the factoring fee for that invoice.

- Setup Fees: Some factoring companies charge an initial setup fee, particularly for new clients, to cover the cost of onboarding and credit checks. These fees are often negotiable and can range from a few hundred to a few thousand dollars, depending on the agreement.

Recourse vs. Non-Recourse Factoring

There are two main types of factoring: recourse and non-recourse.

- Recourse Factoring: In this arrangement, your business is responsible if a customer doesn’t pay the invoice. Since you bear more risk, recourse factoring generally has lower fees.

- Non-Recourse Factoring: With non-recourse factoring, the factoring company takes on the risk of non-payment, so if your customer defaults or goes bankrupt, the factoring company absorbs the loss. Because they take on more risk, non-recourse factoring tends to have higher fees, usually two or three percent higher than recourse factoring.

How Costs Add Up

Factoring costs can vary significantly based on the terms of the agreement and your industry. While it’s easy to focus on the factoring fee alone, it’s important to consider all potential charges. That said, factoring is often more flexible and faster than traditional financing, so the fees can be well worth the benefit of immediate cash flow.

Boosting Business Growth Through Factoring

Invoice factoring doesn’t just solve short-term cash flow problems. It can also be a powerful tool for business growth. By turning unpaid invoices into immediate cash, factoring gives you the flexibility to reinvest in your business quickly, allowing you to capitalize on new opportunities and scale faster. Additionally, the impact of factoring on the cash cycle can be significant, as it shortens the time between issuing invoices and receiving payments, keeping your operations moving smoothly.

Investing in New Projects

One of the biggest challenges for growing businesses is the need to reinvest in new projects, whether that’s launching a new product, expanding services, or entering a new market. These projects often require significant upfront costs, from research and development to marketing and hiring.

Factoring provides you with immediate access to cash that can be reinvested directly into these growth initiatives. Instead of waiting for clients to pay, you can use the funds to hire new staff, scale your operations, or kick off a marketing campaign without delays.

Purchasing Inventory to Meet Demand

Businesses in industries like retail, wholesale, and manufacturing often struggle with maintaining the right level of inventory to meet demand. Whether it’s seasonal spikes or fulfilling large orders, having the necessary capital to purchase raw materials or finished products can make or break a business’s ability to seize growth opportunities.

With factoring, you can unlock cash tied up in your unpaid invoices and use it to stock up on inventory, ensuring you have enough on hand to meet customer demand. This not only helps you keep up with current orders but also positions you to take on larger contracts or bulk orders in the future.

Expanding Operations

Growth often requires expanding your operations—whether that’s opening a new location, upgrading equipment, or increasing production capacity. However, these investments typically require significant capital, and waiting on slow-paying customers can delay expansion plans.

Factoring gives businesses the immediate cash they need to reinvest in expansion without taking on debt. You can use the funds to hire additional staff, buy new equipment, or even open a second location, all while maintaining a healthy cash flow.

Taking Advantage of Early Payment Discounts

Many suppliers offer discounts for early payments, typically around two percent if paid within 10 days. While this may seem small, it adds up quickly, especially if you’re purchasing materials or products in large quantities. However, taking advantage of these discounts requires having enough cash on hand to pay suppliers quickly.

Factoring gives you the liquidity to pay suppliers early and take advantage of these discounts. Over time, this can lead to significant savings, which can be reinvested into your business. Plus, paying suppliers early can strengthen relationships and position your company as a reliable partner, potentially leading to more favorable terms in the future.

Supporting Marketing and Sales Growth

Marketing is often one of the first areas to suffer when cash flow is tight, yet it’s also one of the most critical investments for business growth. A strong marketing campaign can drive new customers, expand your brand presence, and ultimately lead to increased sales.

By factoring invoices, you can free up cash to reinvest in marketing campaigns, new product launches, or sales initiatives. This enables you to grow your customer base and increase revenue without having to wait for customers to pay their invoices.

Start Factoring for Capital Efficiency Today

If you’re interested in improving cash flow with factoring, we’re happy to match you with a factoring company that understands your needs and offers competitive rates. To get started, request a complimentary factoring quote.

Factoring for Capital Efficiency FAQs

How can businesses overcome cash flow challenges with factoring?

Many businesses face cash flow challenges due to delayed customer payments, long payment cycles, or seasonal fluctuations. Factoring provides a solution by allowing businesses to convert unpaid invoices into immediate cash. This process helps companies maintain operational stability, cover expenses like payroll and inventory, and avoid borrowing. In essence, overcoming cash flow challenges with factoring is about bridging the gap between when invoices are issued and when payments are received, ensuring businesses always have the working capital they need.

How does factoring provide quick access to working capital?

Factoring offers businesses quick access to working capital through factoring by converting unpaid invoices into cash, often within 24 to 48 hours. Instead of waiting 30, 60, or even 90 days for customers to pay, businesses can sell their invoices to a factoring company and receive immediate funds. This rapid access to cash helps cover day-to-day operational expenses like payroll, inventory purchases, and overhead, ensuring that the business maintains financial stability without having to take on debt or delay growth opportunities.

How does invoice factoring support business growth?

Invoice factoring and business growth go hand-in-hand, as factoring provides the necessary cash flow to reinvest in key areas of the business. By converting unpaid invoices into immediate cash, companies can fund expansion projects, purchase new inventory, hire additional staff, or invest in marketing without waiting for customers to pay. This consistent flow of capital allows businesses to seize new opportunities and scale operations more effectively, supporting both short-term and long-term growth goals.

What should businesses consider when evaluating factoring companies for capital management?

When evaluating factoring companies for capital management, businesses should consider several key factors. These include the fees charged by the factoring company, the percentage of the invoice value advanced upfront, and the overall terms of the agreement. It’s also important to assess the company’s reputation, customer service, and their ability to handle your industry-specific needs. The right factoring partner will not only provide immediate cash flow but also support your long-term financial management by helping optimize capital efficiency.

How should businesses approach a cost-benefit analysis of invoice factoring?

Conducting a cost-benefit analysis of invoice factoring is essential to determine if it’s the right solution for your business. Start by calculating the factoring fees, which typically range from one to five percent of the invoice value, and weigh this against the benefits of immediate cash flow. Consider how quickly you need access to cash, the potential savings from avoiding late payment penalties or missed opportunities, and how it compares to other financing options. If the benefits of improved cash flow and growth outweigh the fees, factoring could be a cost-effective choice for your business.

What types of businesses benefit most from invoice factoring?

Businesses that often experience delayed customer payments, long payment cycles, or fluctuating cash flow benefit most from invoice factoring. Industries like trucking, manufacturing, staffing, and construction frequently use factoring because they have significant operational costs and need immediate cash to cover expenses. Companies that offer long payment terms to customers or those with growing demand but limited working capital also find factoring helpful. Additionally, small businesses and startups with limited credit history can benefit, as factoring relies on the creditworthiness of their customers, not the business itself.

How does invoice factoring compare to other financing options?

Invoice factoring offers faster access to cash compared to traditional loans or lines of credit. Unlike loans, factoring doesn’t require credit checks or repayment schedules—businesses sell their unpaid invoices for immediate cash. It’s also more flexible than loans, which provide a lump sum, while factoring provides ongoing cash as invoices are generated. Compared to merchant cash advances, factoring usually comes with lower fees and less risk. However, factoring fees can be higher than traditional loan interest rates, so businesses should weigh the cost of factoring against the speed and flexibility it offers.

Can invoice factoring help with managing seasonal cash flow fluctuations?

Yes, invoice factoring is an effective solution for managing seasonal cash flow fluctuations. Businesses that experience peak sales seasons followed by slow periods, such as retail, agriculture, and manufacturing, can use factoring to stabilize cash flow during off-seasons. Factoring allows businesses to convert unpaid invoices into immediate cash, even when revenue dips, helping them cover operational expenses, purchase inventory, and maintain payroll. By factoring invoices during busy periods, companies can build up a cash reserve to carry them through slower months, ensuring consistent liquidity year-round.

Is invoice factoring a good option for startups or small businesses?

Yes, invoice factoring can be a great option for startups or small businesses, especially those with limited credit history. Factoring is based on the creditworthiness of the startup’s customers, not the business itself, making it accessible for companies that may not qualify for traditional loans. It provides quick access to cash without taking on debt or requiring collateral. Startups can use the funds to cover expenses, invest in growth, or take on new projects without worrying about delayed payments. However, businesses should assess the fees associated with factoring to ensure it's cost-effective for their situation.

How quickly can businesses receive funds through invoice factoring?

Businesses can typically receive funds through invoice factoring within 24 to 48 hours after submitting their unpaid invoices to the factoring company. Some factoring companies even offer same-day funding, depending on the agreement and the industry. The quick turnaround makes factoring an ideal option for businesses that need immediate access to working capital to cover operational expenses, payroll, or unexpected costs. The speed of funding depends on factors like the factoring company’s process, the size of the invoices, and the creditworthiness of the customers involved.

About Invoice Factoring Guide

Get an instant funding estimate

Results are estimates based on the calculated rate and the total invoice amount provided.

Actual rates may vary.

Request a Factoring Rate Quote

PREFER TO TALK? Call us at 1-844-887-0300

")